Good news: Queensland’s new payroll tax ruling clarifies that direct-to-practitioner payments are exempt. Bad news: there’s more.

When it comes to payroll tax, direct-to-doctor payments are in and third-party entities are out – at least as far as the Queensland Revenue Office is concerned.

True to its word, the QRO has released an updated ruling on payroll tax in a medical centre context clarifying scenarios where payroll tax may not be applicable.

This version, which runs to almost 30 pages, replaces the 16-page ruling published in December.

Examples 12 and 13, both of which are new additions to the document, appear to confirm what the RACGP and AMA predicted last week: that when a patient pays the doctor their Medicare benefit or out-of-pocket fee directly, it won’t be counted as wages by the state.

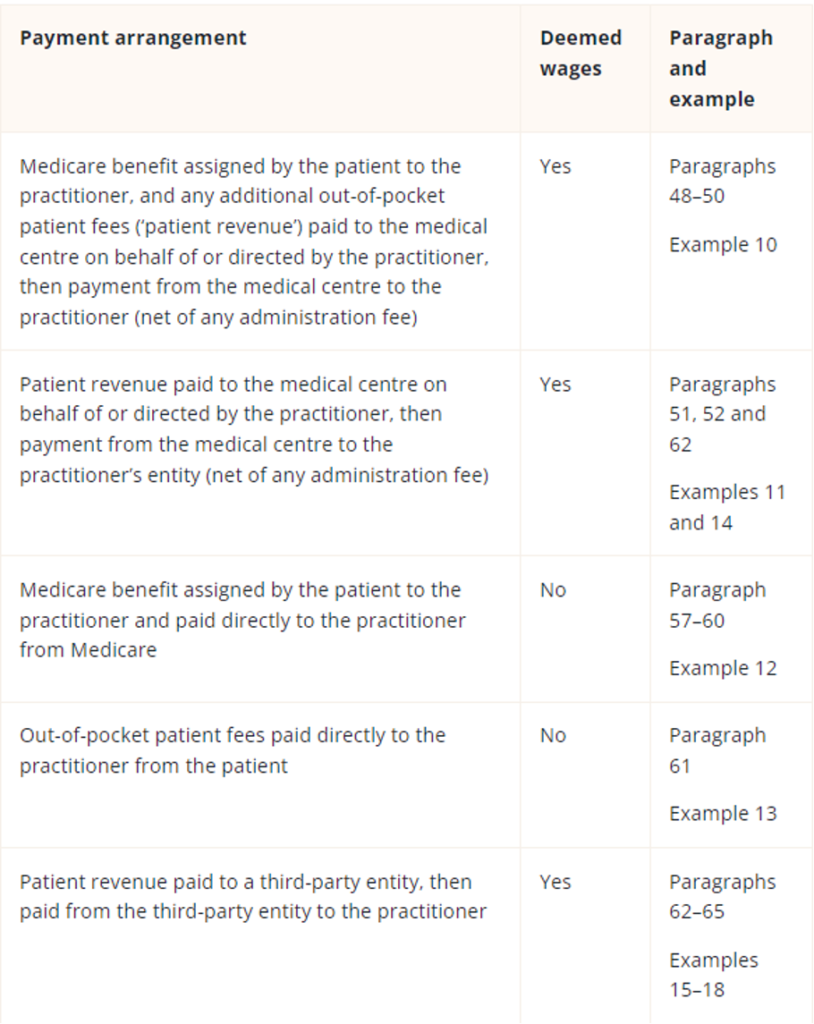

This will apply even where the medical centre is found to be the employer under section 13C of Queensland’s Payroll Tax Act 1971 and the doctor is found to be the employee under section 13D and when no exemptions apply.

The brilliance here comes down to the fact that the amount of payroll tax to be paid is calculated as a percentage of wages.

To put it all together – the QRO could audit a medical centre and find that its contracts with doctors are “relevant contracts” and that it therefore is liable to pay payroll tax. But if all the doctors contracted with that practice have been receiving all their income directly from patients, then there will be no wages to pay payroll tax on: 5% of $0 is still $0.

This only works within very narrow parameters.

As laid out in examples 14 through 18, channelling the money through any third-party accounts will create what the QRO calls “deemed wages”, raising that $0 figure and incurring payroll tax.

This includes scenarios where the patient’s payment goes to a business entity or trust wholly owned by the practitioner which then distributes fees to the doctor and to the practice.

It also includes scenarios where the patient payment goes to an entity or trust owned by the practice.

Caption: Summary of whether certain payments to the practitioner are considered deemed wages. Source: QRO.

William Buck head of health services Paul Copeland told The Medical Republic that the ruling’s position on doctors using wholly-owned businesses or trusts was “unexpected” but ultimately not impossible to work with.

“Some doctors are going to jump up and down and say ‘no, no, no, I don’t want to get rid of my medical company’ … because there are some doctors that believe a medical company provides them with increased asset protection,” Mr Copeland said.

“That’s not correct. When it comes to medical claims, the medical company doesn’t provide any benefit.

“There are also some doctors who believe that using a company or a trust allows them to distribute their personal services income more widely, which, again, is probably very misinformed.”

While it will be an annoyance, he said, unwinding the use of medical companies will likely have “very minimal impact overall”. It generally costs less than $100 to deregister a company.

Payment flows might be the biggest headline to come out of the updated ruling, but there are also three new attachments with what could prove to be very handy information when it comes to judging whether a practice is liable for payroll tax at all.

The second attachment, which lays out key factors that may indicate that a medical centre has “operational or administrative control” over a doctor was of particular interest to both Mr Copeland and to healthcare accountant David Dahm.

“They’ve highlighted 14 key factors or characteristics that you should be able to take to your lawyer or accountant and [see where you stand],” Mr Dahm told TMR.

Basically, practices now have a checklist to see whether or not it’s likely that the state will see them as a medical centre business or simply a business providing administrative support to a group of doctors.

Being classified as the latter is preferable because it has the potential to get the business out of any liability for payroll tax on contractor doctors.

Overall, Mr Dahm said he was approaching the ruling with caution and did not trust that there was a straightforward or simple solution to payroll tax.

“From experience, it’s never been that simple or that straightforward,” he said.

It’s a good start, he said, but right now it would not be uncommon to find a medical centre collecting patient fees under the same ABN that it uses to pay its reception staff and practice manager.

He also warned against relying on the direct-to-doctor bank account approach without proper legal and accounting advice.

RACGP Queensland chair Dr Bruce Willett told TMR that the full details of the ruling show the government has “made good” on its promise not to pursue practices for payroll tax in scenarios where clinicians receive patient payments directly.

“This is great news for GPs, practice teams, and the patients we care for. The ruling provides practices with greater certainty and a clear path forward, even if it is slightly more of a winding path than we would all ideally like,” he said.

“Nevertheless, it is a great alternative to practices spending valuable time and money fighting this out in the courts.”

FREE Webinar: A guide to tax (state and federal) for medical service centres and GPs

Confused at all the back and forth from medical colleges, MDAs and state revenue offices on what does and doesn’t constitute tax compliance for a tenant doctor and a service entity acting as a landlord for tenant doctors?

This FREE one-hour webinar hosted by The Medical Republic and featuring HealthAndLife principal David Dahm and Hamilton and Bailey solicitor Lukasz Wyszynski, a specialist in medical practice tax, will take you through all the case law and accounting principles that apply to you, including emerging law around ATO obligations for tenant doctors and the latest detailed ruling on payroll tax from the Queensland Revenue Office.