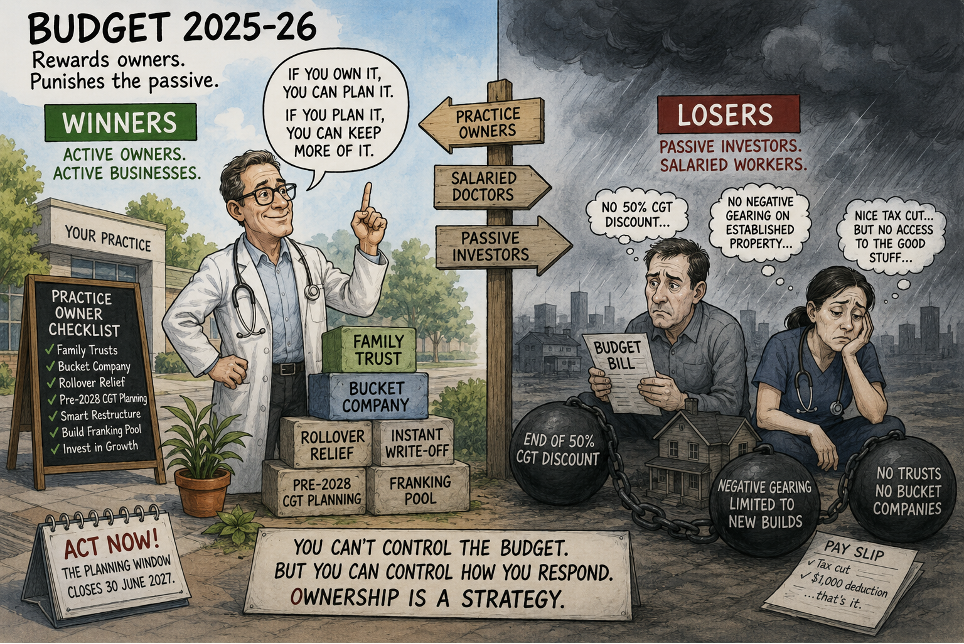

Becoming a practice owner or part-owner is, in many cases, the strongest single response a working GP might make to this budget.

If you own or part-own a practice, distribute through a family trust, run a bucket company, hold investment property, or are planning to sell your practice in the next decade, this budget was about you.

A one-line takeaway from last night’s budget for GPs might be:

It rewards practice owners and part-owners running active businesses, and it punishes two groups: passive investors and salaried workers.

Passive investors lose the 50% capital gains discount; established residential housing acquired after budget night loses negative gearing against wages from July 1 2027.

Salaried workers, including most salaried doctors and registrars, receive modest personal tax cuts and a $1000 instant deduction, but have no access to the structural planning tools (family trusts, bucket companies, rollover relief) that owners and part-owners can use to manage the new regime.

Importantly, and perhaps not immediately obvious, family trusts remain a very good idea for practice owners and part-owners, both for asset protection and for the meaningful tax planning that survives the new 30% floor.

Becoming a practice owner or part-owner is, in many cases, the strongest single response a clinician can make to this budget.

Nothing has been legislated yet and the substantive changes do not commence until 1 July 2027 at the earliest so you have a vital planning window over the next 13 months.

Priority checklist at a glance

Red items need attention in the next six months. Amber items are important within 12 to 18 months. Green items are positive opportunities or items to monitor.

| Priority | Measure | Commences | Who it affects | Action |

| RED | Discretionary trust 30% minimum tax | 1 Jul 2028 | Practice owners with family trusts | Deed reviews now; plan restructure within rollover window |

| RED | CGT 50% discount replaced with indexation plus 30% minimum | 1 Jul 2027 | Anyone with CGT assets | Crystallise eligible gains before 1 Jul 2027 where commercial |

| RED | Negative gearing limited to new builds (established housing) | 1 Jul 2027 (12 May 2026 cut-off) | Property investors | Check contract dates; redirect to new builds |

| RED | Bucket company anti-avoidance | 1 Jul 2028 | Practice owners using bucket companies | Maximise FY26, FY27, FY28 distributions under old rules |

| RED | Multi-owner practices: share class design on restructure | 1 Jul 2027 (rollover) | Multi-owner practices in discretionary or hybrid trusts | Design A/B/C share classes; revisit profit-sharing arrangements |

| AMBER | Sham contracting joint ATO and Fair Work crackdown | Live since March 2026 | All practice owners with contracted doctors | Refresh tenant doctor documentation |

| AMBER | Multi-owner shareholder or unitholder agreement review | Before 30 Jun 2027 | Multi-owner practices retaining their trust | Update profit-sharing formula; document each owner’s economic share |

| AMBER | AML/CTF Tranche 2 commencement | 1 Jul 2026 | Practices handling patient receipts | Confirm scope; AUSTRAC enrolment if in scope |

| AMBER | EV FBT full exemption window closing | 1 Apr 2027 / 1 Apr 2029 | Anyone considering an electric vehicle | Lock in salary packaging before 1 April 2029 |

| AMBER | Bulk Billing Practice Incentive Program continues | Live | GP practice owners | Refresh BBPIP opt-in modelling |

| GREEN | Rollover relief for trust restructure | 1 Jul 2027 to 30 Jun 2030 | Practice owners with discretionary trusts | Use the three-year window for structural transition |

| GREEN | Pre-2028 bucket company franking pool | FY26, FY27, FY28 | Practice owners with bucket companies | Build the franking pool while old rules apply |

| GREEN | $20,000 instant asset write-off made permanent | 1 Jul 2026 | Self-employed practitioners under $10m turnover | Plan capex with confidence |

| GREEN | Loss carry-back for companies | 2026-27 | Companies in transition | Offset losses against prior two years’ tax |

| GREEN | Monthly PAYG instalments option | 1 Jul 2027 | Self-employed with lumpy cashflow | Consider opt-in |

| GREEN | $1,000 instant deduction for work-related expenses | 2026-27 | Salaried practitioners | Built-in tax cut for every working family member |

| GREEN | $250 Working Australians Tax Offset | 2027-28 | Every working Australian | Automatic on lodgement |

| GREEN | 15% (then 14%) second marginal rate | 1 Jul 2026 / 1 Jul 2027 | Every working Australian | Factor into salary review timing |

| GREEN | New build negative gearing | 1 Jul 2027 (permanent) | Property investors going forward | Redirect investment to new builds |

The four structural changes

- The 30% floor on family trusts (from 1 July 2028).

Discretionary trusts will pay a minimum 30% on their taxable income. Beneficiaries receive a non-refundable credit. If the beneficiary’s marginal rate is below 30% (a retired parent, a child at university, a spouse on parental leave), the credit is wasted. The variable income-splitting benefit that has driven family trust planning for forty years is gone for new income from 1 July 2028.

Notably here, trusts continue to be useful for asset protection, succession, and rate compression against the top marginal rate.

- The end of the 50% CGT discount (from 1 July 2027).

The 50% CGT discount for individuals, trusts and partnerships is replaced by cost base indexation plus a 30% minimum tax rate on the indexed gain. Gains accruing before 1 July 2027 keep the existing 50% discount. Pre-1985 assets remain CGT-exempt on gains accruing before that date. Superannuation funds, including SMSFs, are unaffected. For high-growth long-held assets, the pre and post 1 July 2027 difference is 10 to 15 percentage points of effective tax.

- Negative gearing limited to new builds (from 1 July 2027, with a 12 May 2026 cut-off).

Properties held before budget night are grandfathered indefinitely.

Established housing acquired after budget night can only deduct losses against rental income or capital gains, not wages, from 1 July 2027. New builds preserve the full benefit against all income, indefinitely.

- Bucket companies are reset (from 1 July 2028).

The budget paper language on this point is very thin and the question of whether bucket companies remain useful from 1 July 2028 is genuinely unresolved.

On a strict reading, routing trust income through a bucket company under the new rules produces an effective rate of 55% to 60%. But two questions remain open. First, whether the imputation system will be retrofitted to preserve a single layer of taxation (Australia’s imputation system since 1987 has been designed to avoid the double taxation of corporate profits; whether the trustee 30% will flow through as a franking credit or equivalent is not yet known). Second, the related question of what the rules do for a trust that retains its trust form: the trust pays 30% (the company tax rate), with the credit passing through to beneficiaries; for a family on broadly 30% or higher marginal rates, this is closer to a deemed company structure than a catastrophic outcome.

Related

The pre-2028 bucket company strategy survives indefinitely for pre-2028 income, and the next three income years (FY26, FY27, FY28) are the last opportunity to build a refundable franking pool under existing rules.

What this means in dollars

Consider a GP earning $400,000 a year plus $300,000 of service entity profit, with a spouse on parental leave, two adult children at university, and a retired parent in the beneficiary class.

Under current rules, distributions across the five family members produce a family-level effective rate of around 15 to 17% on the service entity profit.

From 1 July 2028, the same pattern produces an effective rate of around 34%. The annual cost of inaction is in the order of $50,000.

If the same family restructures the trust to a company under the rollover relief available from 1 July 2027, the effective rate falls back toward 10% to 12%.

The mechanism is the destination company’s franking account flowing to low-marginal-rate shareholders.

If the franking pathway is broken by exposure draft rules, this number changes. As noted under measure four above, the imputation question is genuinely open.

Who is actually affected, and who is not

The dollar example above is deliberately the worst case. For a high net worth family where all beneficiaries are practitioners or working professionals already on 30% or higher marginal rates, the budget is relatively neutral: the trustee pays 30%, the beneficiaries absorb the credit, the income-splitting benefit they were receiving was modest, and the absolute dollar impact of losing it is small.

The families most affected are those splitting to retired parents on zero marginal rate, adult children at university on low marginal rates, and a spouse temporarily out of the workforce.

For the university group, the impact is temporary: a child at university typically moves to full-time work within four to five years, the marginal rate rises, and the splitting benefit was always going to wash out.

The budget brings the wash-out forward, not changes the lifetime outcome.

The retired parent group is more enduringly affected, but the pre-2028 bucket company franking pool partially compensates: $50,000 of franked dividends with a refundable credit produces roughly the same after-tax outcome as a $50,000 trust distribution. The franking pool can be built across FY26 to FY28 and drawn down over the next decade.

Again, family trusts remain useful for significant tax planning, separately from income splitting.

Rate compression against the 47% top marginal rate is valuable for any beneficiary at lower rates. Trust losses continue to be quarantined within the trust.

The capital gains discount on pre 1 July 2027 gains is preserved on existing trust assets. And the asset protection and family law arguments below are unrelated to the tax change.

The right framing of the budget is not that family trusts are dead. It is that the income-splitting amplifier has been turned down. The trust itself remains a sophisticated wealth, succession and asset protection vehicle.

A common misconception

Some GPs will assume their clinical earnings are now subject to the 30% trust floor. They are not.

Personal services income (clinical fees earned by a GP, specialist, or allied health professional) has been restricted under Part 2 42 of the Income Tax Assessment Act 1997 since 2000 and is attributed back to the practitioner personally at full marginal rate regardless of structure.

The new trust rules sit above this. What they affect is the genuine business profit of a service entity, typically twenty to thirty% of service fees under a properly documented tenant doctor arrangement.

Tax is not the only consideration

Before any practice owner commits to a trust-to-company restructure, it is essential to remember why family trusts exist. The tax benefit is incidental. The structural benefits are not.

Asset protection is the most important non-tax benefit.

Discretionary beneficiaries hold a mere expectancy in trust assets, not an enforceable entitlement.

In a family law dispute, the spouse of a beneficiary cannot claim a share of trust assets because there is no share to claim. The position is materially different for a shareholder in a company, who holds an enforceable property right in their shares.

If you are concerned about who one of your adult children might marry, or about marriage breakdown risk of any current spouse, a discretionary trust offers protection that a company structure does not replicate.

The protection has limits, particularly in inheritance disputes brought by your own children. Every Australian state and territory has a family provision regime: New South Wales is the most expansive example (the notional estate doctrine under the Succession Act 2006 (NSW) can draw trust assets back into a deceased parent’s estate to meet a family provision claim); South Australia has parallel legislation in the Inheritance (Family Provision) Act 1972 (SA); Victoria, Queensland, Western Australia, Tasmania, the ACT and the Northern Territory each have their own equivalents. A discretionary trust is a strong shield against the spouse of a beneficiary, but a much weaker shield against the children of the principal.

Creditor protection matters too.

A medical or allied health principal carries personal liability exposure even with limited liability structures in place.

Family wealth held in a discretionary trust sits outside the practitioner’s personal asset pool; a company structure with the practitioner as shareholder offers shallower protection.

The post-2028 incidental tax benefit reduction may also be temporary.

Tax policy moves in cycles. There are still strong, viable reasons to keep your family trust, and to absorb the modest annual cost of the 30% floor, in exchange for asset protection that company structures cannot replicate.

The right answer differs for every family.

Multi-owner practices: share class design is critical

A specific complication applies if your practice is owned by a discretionary or hybrid trust and there is more than one owner family.

When such a trust is converted to a company under the rollover relief, the future profit-sharing arrangement is fixed by the share register. Ordinary shares pay pro-rata to shareholding. If 50/50 shares are issued but real economic contribution is 60/40, the company pays 50/50 and the doctors will need to true that up outside the company, raising Division 7A and PSI risks.

The way through this is to design different share classes on conversion. A class shares for Family One, B class shares for Family Two, with dividend rights set out in the constitution to mirror the economic arrangement the owners actually want. This permits differential dividend declarations year on year with formal company law substance.

Before any multi-owner practice commits to the rollover, every implicit profit-sharing arrangement in the existing trust needs to be re-checked. If those arrangements are not already fixed by the deed, they are about to become fixed by the share register. A poorly designed share class structure is significantly harder to fix after conversion than a poorly designed trust deed is to vary.

The sham contracting backdrop and the rollover relief

The joint ATO and Fair Work Ombudsman sham contracting crackdown that began in March 2026 continues to be funded through to 2028-29.

Data matching across TPAR, Single Touch Payroll, ABN records, and tax returns flags contractors who work almost exclusively for one business. Fair Work penalties can reach $495,000 per contravention for larger practices.

PAYG withholding, Super Guarantee Charge, retrospective payroll tax, and WorkCover stack on top. Post Bird v Department of Education and Training [2024] HCA 41, vicarious liability flows back to the practice entity and its directors personally. A practice that restructures under the trust rollover relief without first refreshing the tenant doctor documentation is opening two fronts at once.

From 1 July 2027 to 30 June 2030, discretionary trusts can be restructured into fixed trusts or companies with no federal income tax or CGT consequences. This is the planning window.

The state stamp duty position is more favourable than many clients assume: New South Wales, Victoria, South Australia, Tasmania, the ACT and the Northern Territory have all abolished stamp duty on business assets; only Queensland and Western Australia still levy duty on goodwill and intellectual property.

For practices that lease rather than own their premises, the practical stamp duty cost of restructure is nominal.

What to do before 30 June 2027

1. Commission a deed review on every trust in your structure now. For multi-owner practices, the second question is equally important: are the profit-sharing arrangements between owner-families already fixed, or implicit and discretionary? Any implicit arrangement that survives into a company structure must be reflected in the share class design.

2. Maximise legitimate distributions to your bucket company in FY26, FY27 and FY28. Every dollar distributed and franked builds a refundable pool that survives the new regime indefinitely. Section 100A and Division 7A discipline must be tight.

3. Model your CGT position on every significant asset you might dispose of in the next ten years.

4. Review any property purchases in progress. Contracts exchanged before 12 May 2026 are grandfathered.

5. Refresh the structural documentation on your tenant doctor arrangement. Service agreements, fee determination evidence, doctor autonomy, and the separation of doctor and practice branding all need to be current.

6. Wait for the exposure draft before committing to irreversible restructures. Equally important, work through the non-tax considerations (asset protection, family law exposure, creditor protection) before any restructure decision.

A closing thought

The five biggest questions for any practice owner are: who is in your beneficiary class and what are their marginal rates over the next decade; what does the deed of every trust in your structure actually say; what asset disposals are likely in the next five to ten years; which entity is the right one to own your future income; and what asset protection, family law, and creditor exposure considerations sit alongside the tax outcome.

The budget has not changed the importance of those questions. It has changed the answers on tax. The answers on everything else are unchanged.

Note: This article is a high-level summary written within hours of Budget night. Significant mechanics remain subject to consultation through the exposure draft expected later this year and the legislation that follows. The Budget papers themselves leave many points of detail unclear, including the critical question of how the new 30% trustee tax will interact with the imputation system. The devil is in the detail. Do not act on this article without advice from a qualified accountant and a qualified lawyer specific to your circumstance,

David Dahm is the principal of Health and Life, a chartered accounting and healthcare advisory firm.