Queensland seems to have kiboshed automated payment solutions while the ACT suggests flows won’t make any difference.

Two payroll tax clarifications, one from the Queensland Revenue Office and one from the ACT, are likely to add some confusion to the payroll tax debate.

The QRO ruling on payment flows now seems to directly contradict the ACT ruling, and the updated QRO position looks like it is ruling out automated patient-to-tenant-doctor banking and software solutions, without which practices may not be able to afford to change how the money flows.

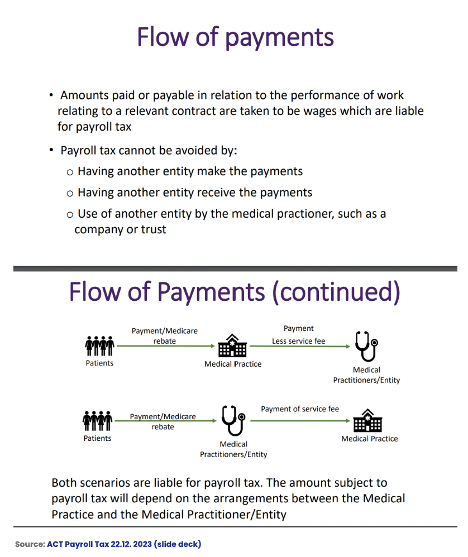

First the ACT clarification, which appeared in a presentation from the ACT Revenue Office late last year.

The above diagram looks like it rules out what the QRO ruled in late last year, saying payments flowing from patients to the doctor or the doctor’s entity first and a commission then being remitted to an administrative landlord will still attract payroll tax.

The RACGP came out at the time of last year’s QRO ruling and said it was a form of victory for doctors in that state because it meant that although there may be other elements that suggest a practice should pay payroll tax on GP income, if the payments flowed in from patient to tenant doctor first, then that money won’t be payroll-taxed.

This implied that in many practices the problem could be solved by restructuring how the money flowed between a tenant doctor in a leased centre (note: we are not calling it a “medical practice”) and that tenant doctor’s patient.

Having two seemingly contradicting positions like this might prove awkward for all state and territory revenue offices if, as some corporate-backed practices in Victoria are threatening, some practices start taking cases to court to test intepreations and rulings legally.

So far payment flows to medical centres first have been tested in court in Thomas and Naaz and that case has suggested strongly that such an arrangement could make the monies flowing liable to payroll tax – it is still not entirely clear because in this case the doctor contracts were a big part of the problem in association with the payment flows.

But so far there has been no formal legal ruling on whether flows directly to a tenant doctor first might make those monies not liable to be captured in payroll tax. All that has happened is that the QRO has said that if the money flows this way, its interpretation is that it won’t be captured.

The RACGP has been pushing for all the states to adopt the comprehensive Queensland ruling in the hope that it will bring much greater clarity to owners on how to invest in and structure their businesses, and provide a simple way of pushing most of the money flow out of the payroll tax net.

But in a potentially serious blow to that strategy, the QRO’s updated ruling this week seems to be knocking out of play any automated banking or software solution designed to make the process of patient-to-doctor payment flows administratively easy and less expensive to set up and administer.

The important part of the updates owners are going to need to look at are paragraphs 62 and 63.

Paragraph 62 says: “… if certain banking arrangements in fact involve an initial payment by the patient followed by one or more further payments by the medical centre or a third party, then these further payments may be deemed wages”.

The problem potentially here for the automated solutions in market is the term “third party”. There is an implication here that there can’t be anything in between the patient and doctor at all if the money flows are to be excised from payroll tax assessments.

Paragraph 63 says: “Close consideration must be given to whether, under the relevant contract, the practitioner’s ability to access the patient revenue paid to them is conditional on the approval or direction of the medical centre … Each payment arrangement will be considered on a case-by-case basis to determine whether the payment(s) are deemed wages.”

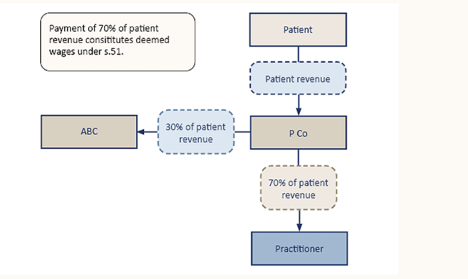

The diagram of flows from the example provided in the ruling in paragraph 65 also suggest this may now be a problem for owners:

“P Co”, the QRO’s fictional third-party clearing house, looks a lot like a series of automated solutions now being offered by some of the big banks and aligned software vendors. P Co is any entity that holds the money outside of the medical centre account (ABC) and the doctor’s account (practitioner). It is meant to overcome the huge administrative burden and expense of a practice attempting to set up and follow payments from every patient to every tenant doctor.

It’s pretty confusing (as usual), so owners will need to read it and get their accountants to read it as well and see if the automated solutions that are being offered are still in play.

Commenting on both the ACT and QRO clarifications, Health&Life principal David Dahm says that in a manner both clarifications are “red herrings” in terms of getting out of having to pay payroll tax or income tax.

“The reality is that you’re either an administrative entity with doctors using your facilities as genuine tenants, and your whole setup meets that test, or you are a ‘medical centre’ – and if you are a medical centre then payment flows to patients first will not ultimately matter anywhere,” he tells TMR.

“The Queensland ruling is comprehensive and very useful but even it consistently refers to ‘medical centres’ in its wording, which is possibly proving quite confusing for a lot of owners.

“If you really don’t want to pay payroll tax you need to be running and administrative centre for offices and services for independent doctors i.e. tenant doctors who are leasing your space and services as genuine tenants.

“What the QRO is doing in its clarification last week, which targets independent payment flow solutions by some banks and software vendors, is reminding everyone that it’s about what the whole setup is, not just about one or two things that make you look like you’re not a medical practice.

“If you’re an administrative business e.g. a service trust or company providing space and support services only to tenant doctors, every aspect of your operation and the doctors must follow that principle.

“It can and is being done by more and more groups, but the reality of how broad-ranging the SRO rulings are still probably has not sunk in with some owners and possibly some corporates.”

Nonetheless, as far as the QRO update is concerned, everything is still a ruling. It has not been tested in court, however many of the examples used are based on court precedent.

Related

Dahm says it is a myth that every point has to be court-tested.

“It is clear that the SRO’s and income tax offices are sufficiently confident of a successful outcome or they would not publish a ruling,” he says.

He says entities should stop calling themselves a “medical centre” and running like one, instead of an “administrative business”.

“If you really do this you will kill three birds with one stone: payroll tax, income tax and the new Fair Work contractor laws. You have to look at all and not just some of the issues at play.”

But if the QRO is seeking to knock out automated banking solutions to the flow problem, the question for the RACGP and the AMA should obviously be, why?

Dahm thinks it’s probably because they are trying to send a message that piecemeal solutions will not work.

“It has to be real and that means a lot of ducks in a row, not just getting yourself a new payment flow solution from a bank,” he said.